24 August 2019|The Interregnum|Michael Roberts

Long time City economist Michael Roberts writes that the decline in the rate of profitability in the US economy (as well as others) is leading to a recession. Roberts, using a Marxist critique, argues that Keynesian, Post-Keynesian, and Modern Monetary Theorists – while well meaning – are incorrect in their belief that a government-backed stimulus will either prevent a recession, or result in recovery from one.

Featured image via Mohamed Elmaazi

EDITOR’s NOTE: Michael Roberts (pseudonym) has been working in the City of London for over 30 years and is author of several books, The Great Recession and the Long Depression. He has a blog providing a Marxist view on economics and the world economy at thenextrecession.wordpress.com.

This article was first published in Michael Roberts Blog on 24 August 2019. It is republished here with permission of the author. The Interregnum has added subheadings to this article.

With perfect timing, just as the summit meeting of the leaders of the top capitalist economies (G7) met in Biarritz, France, China announced a new round of tariffs on $75bn of US imported goods. This was in retaliation to a new planned round of tariffs on Chinese goods that the US planned for December. US President Trump reacted angrily and immediately announced that he was going to hike the tariff rates on his existing tariffs on $250bn of Chinese goods and impose more tariffs on another $350bn of imports.

US trade war with China triggers global slowdown

The US president also said he was ordering US companies to look for ways to scrap their operations in China. “We don’t need China and, frankly, would be far better off without them,” Mr Trump wrote. “Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME and making your products in the USA.”

This intensification of the trade war naturally hit financial markets; the US stock market fell sharply, bond prices went up as investors looked for ‘safe-havens’ in government bonds and the crude oil price fell as China was going to impose a reduction on US oil imports.

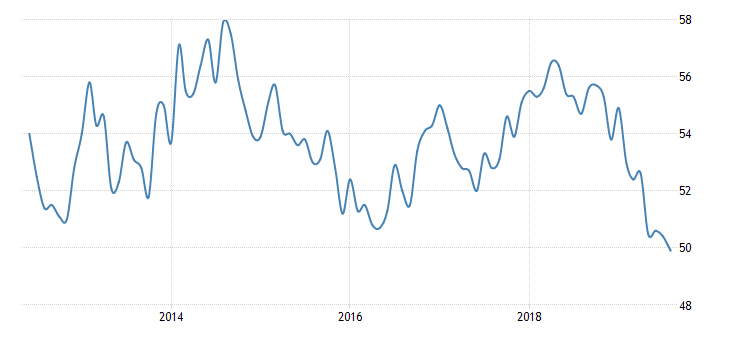

These developments came only a day after the latest data on the state of the major capitalist economies revealed a significant slowdown. The US manufacturing activity index (PMI) for August came in below 50 for the first time since the end of the Great Recession in 2009.

Indeed, the US, Eurozone and Japanese indexes are below 50, indicating a full-out manufacturing recession is here now. And the ‘new orders’ components for each region was even worse – so the manufacturing index is set to fall further. Up to now, the service sectors of the major economies have been holding up, thus avoiding an indication of a full-blown economic slump. “This decline raises the risk that weakness in manufacturing may have begun to spill over to services, a risk that could generate a sharper-than-expected weakening in US and global labor markets.” (JPM). Overall, JP Morgan reckons the world economy is growing at just a 2.4% annual pace – close to levels considered a ‘stall speed’ before outright recession.

Despite all his bluster about how well the US economy is doing, Trump is worried. In addition to attacking China, he also launched again into criticising US Fed chair Jay Powell for not cutting interest rates further to boost the economy, calling Powell as big an “enemy” of the US economy as China!

Powell had just been speaking at the annual summer gathering of the world’s central bankers in Jackson Hole, Wyoming. In his address, he basically said that there was only so much monetary policy could do. Trade wars and other global ‘shocks’ could not be overcome by monetary policy alone. Powell’s monetary policy committee is split on what to do. Some want to hold interest rates where they are because they fear that too low interest rates (and everywhere they are going negative) will fuel an unsustainable credit boom and bust. Others want to cut rates as Trump demands to resist the recessionary forces descending on the economy. Powell bleated that “We are examining the monetary policy tools we have used both in calm times and in crisis, and we are asking whether we should expand our toolkit.”

Monetary policy isn’t working

The trouble is that the central bankers at Jackson Hole are realising, as had already become obvious, that monetary policy, whether conventional (cutting interest rates) or unconventional (printing money or ‘quantitative easing’) was not working to get economies out of low growth and productivity or avoid a new recession.

Many of the academic papers presented to the central bankers at Jackson Hole were laced with pessimism. One argued that bankers needed to coordinate monetary policy around a global ‘natural rate of interest’ for all. The problem was that “there is considerable uncertainty about where the neutral rate really lies” in each country, let alone globally. As one speaker put it: “I am cautious about using this impossible-to-measure concept to estimate the degree of policy divergence around the world (or even just the G4)”. So much for the basis of most central bank monetary policy for the last ten years.

Another paper pointed out that “monetary policy divergence vis-a-vis the U.S. has larger spillover effects in emerging markets than advanced economies.” So “domestic monetary policy transmission is imperfect, and consequently, emerging markets’ monetary policy actions designed to limit exchange rate volatility can be counterproductive.” In other words, the impact of the Fed’s policy rate and the dollar on weaker economies is so great that smaller central banks can do nothing with monetary policy, except make things worse!

Mark Carney: dominance of US Dollar is a threat to global economy

No wonder, Bank of England governor Mark Carney in his speech took the opportunity before he leaves his post to suggest that the answer was to end the rule of dollar in trading and financial markets. The US accounts for only 10 per cent of global trade and 15 per cent of global GDP but half of trade invoices and two-thirds of global securities issuance, the BoE governor said. As a result, “while the world economy is being reordered, the US dollar remains as important as when Bretton Woods collapsed” in 1971. It caused too much imbalances in the world economy and threatened to bring down weaker emerging economies which could not get enough dollars. It was time for a global fund to protect against capital flight and later a world monetary system with a world money! Some hope! But he showed the desperation of central bankers.

The impending global recession has also concentrated the minds of mainstream economics. A division of opinion among mainstream economists has broken out over what economic policy to adopt to avoid a new global recession. Orthodox Keynesian, Larry Summers, former US treasury secretary under Clinton and Harvard professor, has argued the major capitalist economies are in ‘secular stagnation’. So he reckons monetary easing, whether conventional or unconventional, won’t work. Fiscal stimulus is needed.

On the other hand, Stanley Fischer, formerly deputy at the US Fed and now an executive of the mega investment fund, Blackrock, reckons that fiscal stimulus won’t work because it is not ‘nimble enough’ ie takes too long to have an effect. Also, it risks driving up public debt and interest rates to unsustainable levels. So monetary measures are still better.

Michael Roberts: Monetarists and Keynesians are wrong

The post-Keynesians and Modern Monetary Theory economists got very excited because Summers seemed to agree with them, finally, – namely that fiscal stimulus through budget deficits and government spending can stop ‘aggregate demand’ collapsing. It seems that the consensus among economists is moving to the view that central bankers can do little or nothing to sustain capitalist economies in 2019.

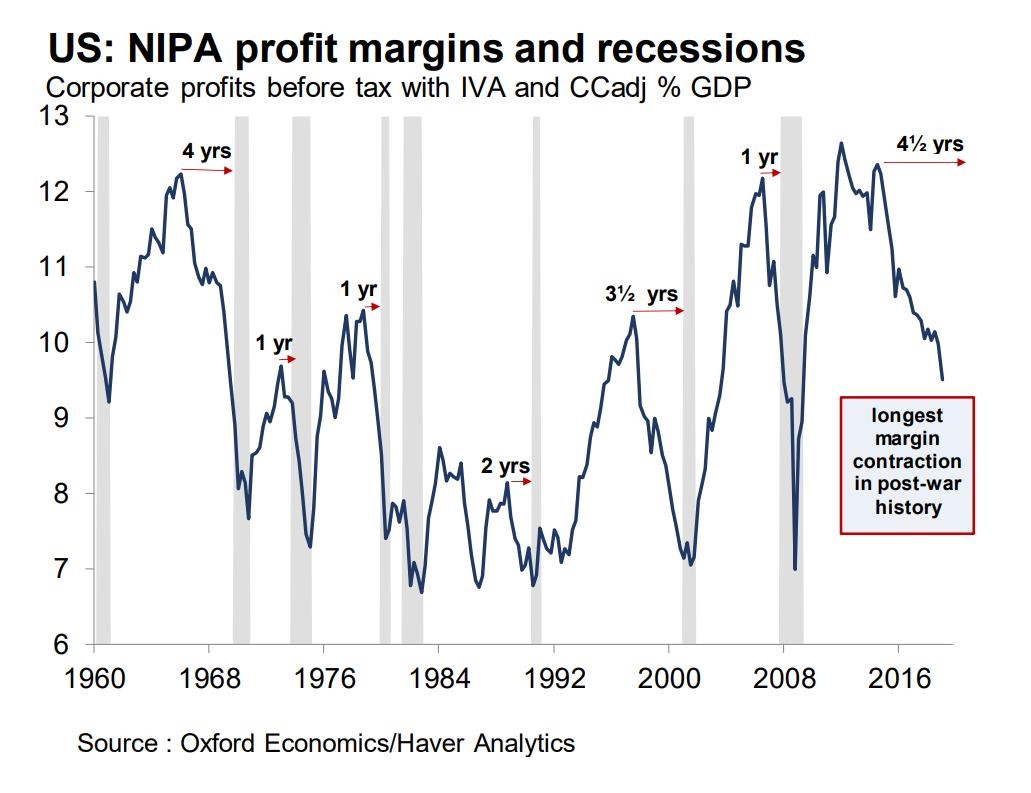

But in my view, neither the ‘monetarists’ nor the Keynesians/MMT are right. Whether more monetary easing and fiscal stimulus, nothing will stop the oncoming slump. That’s because it is not to do with weak ‘aggregate demand’. Household consumption in most economies is relatively strong as people continue to spend more, partly through extra borrowing at very low rates of interest. The other part of ‘aggregate demand’, business investment is weak and getting weaker. But that is because of low profitability and now, in the last year or so, falling profits in the US and elsewhere. Indeed, US corporate profit margins (profits as a share of GDP) have been falling (from record highs) for over four years, the longest post-war contraction.

The Keynesians, post-Keynesians (and MMT supporters) see fiscal stimulus through more government spending and increased government budget deficits as the way to end the Long Depression and avoid a new slump. But there has never been any firm evidence that such fiscal spending works, except in the 1940s war economy when the bulk of investment was made by government or directed by government, with business investment decisions taken away from capitalist companies.

The irony is that the biggest fiscal spenders globally have been Japan, which has run budget deficits for 20 years with little success in getting economic growth much above 1% a year since the end of the Great Recession; and Trump’s America with his tax cuts and corporate tax exemptions in 2017. The US economy is slowing down fast, and Trump is hinting at more tax cuts and shouting at Powell to cut rates. In Europe, the European Central Bank is preparing a new round of monetary easing measures. And even the German government is hinting at fiscal deficit spending.

So we shall probably get a new round of monetary easing and fiscal stimulus measures, to satisfy all parts of mainstream and heterodox economics. But they won’t work. The trade and technology war is the trigger for a new global slump.